Comparing daily closing prices of the XAO with standard distributions

Introduction There are many reasons, both sociological and technical, why capital markets are an interesting application–domain for sonification. Sociologically, they have become a powerful, some might say almost religious, contemporary force, even as their overtly emotional expressive open-outcry marketplaces have become, or are quickly becoming, virtualised gatherings of disembodied screen traders. Sonification of the activities of these markets thus functions as a form of re-embodiment.

While such sociological considerations are interesting, the studies reported here are more pragmatic and descriptive. Despite intensive study, a comprehensive understanding of the structure of capital markets exchange trading data remains elusive. For an overview of this issue, see Chapter 5 of Sonification and Information, including more detail of the techniques illustrated here, or just read a brief overview of market data.

The flexibility of money, as with so many of its qualities, is most clearly and emphatically expressed in the stock exchange, in which the money economy is crystallized as an independent structure just as political organisation is crystallized in the state. The fluctuations on exchange prices frequently indicate subjective-psychological motivations, which, in their crudeness and independent movements, are totally out of proportion in relation to objective factors.

Georg Simmel. The Philosophy of Money. 1900/1979

Why use sonification? The power of visual representation to enhance and deepen the understanding of phenomena and their abstractions is undisputed. Yet, as with many time-domain processes, visual representation does not always reveal the structure of the data. In The (mis)Behavour of the Markets Benoit Mandelbrot emphasises the difficulty, even impossibility, of distinguishing the difference between real market data and computer-generated Brownian motion using graphs.

This leads to a sonification question: Are there ways of presenting trading data that enable its structural characteristics to be perceived aurally? To explore that question, we sonify the XAO, an Australian market index, along with a computer-generated statistical analogue of it for comparison.

The ASX All-Ordinaries Index (XAO)

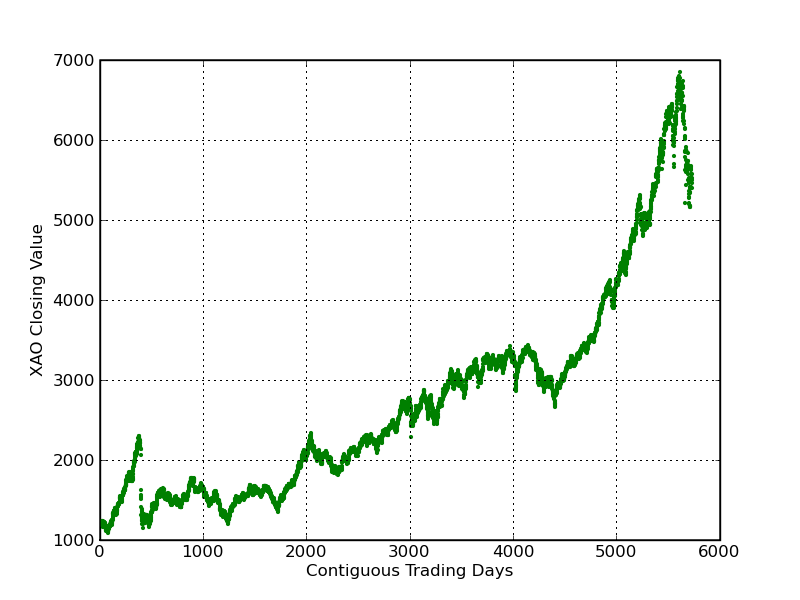

Figure 1. 22 years of daily closing prices of the ASX-XAO.

The dataset chosen is twenty-two years (21April 1986 to 18 April 2008) of the daily closing price of All Ordinaries Index (ticker XAO) of the Australian Securities Exchange (ASX). The XAO is the broad Australian market indicator, a composite of the 500 largest companies, weighted by capitalisation, which are listed on the exchange. Figure 1 is a graphical representation of this dataset.

Net Returns As the value of XAO increase roughly exponentially over time, the technique chosen here is to convert the dataset in to a series of net-returns, or ratios of successive value differences. For an asset whose price changed from p(t) at time t to p(t+dt) at time t+dt, the linear net returns Rnet are defined as (p(t+dt) - p(t))/p(t).

Figure 2. Graph of the Net Returns of the XAO dataset.

Figure 2 is a graphical representation of these net returns. The insert is an amplification of the dotted sesction containing a very negative return–that of 20 October 1987 (“Black Tuesday"), the largest one-day percentage decline in stock market history.

Sonification of Net Returns Clearly, there are a number of possible mappings of his dataset into sound. Because it basically oscillates around zero, it is possible to audify it directly. However, for this discussion we map it using a very simple technique we call homomorphic mapping sonification in which the zero is assigned a centre frequency and the positive and negative returns are used to modulate that frequency within a fixed range.(For an exposition of using direct audification, see Chapter 5 of Sonification and Information.)

Larger changes in pitch indicate larger changes, i.e. higher volatility, in $value. Play XAO net returns sonification (7.6 Mb MP3 file).

Here is a sonification of uniformly random net returns to compare with the market net returns. Play Random Net Returns sonification (7.6 Mb MP3 file).

Here is a sonification of a set of normally distributed random returns, with the same mean and standard deviation as the original set of market returns. Play Gaussian Net Returns sonification (7.6 Mb MP3 file).

How can the sonification of net-returns be characterised? One way is to compare it those of other known datasets. This leads to a second sonification question:

Can real trading data be distinguished from a stochastic simulation of it? Notice the overwhelming preponderance of small pitch changes (small changes in net returns) with occasional periods of greater volatility. This is even clearer when we compare it to a couple of standard distributions: uniform random, and Gaussian.

Uniform Random (white–noise) In a uniform random, or "white noise" distribution, all net returns all are equally likely.

Gaussian/Normal (Bell-Shaped) Returns In a Gaussian, "normal" or bell-shaped random distribution, the net returns with the greatest frequency are centred round the mean and those furthest away from the mean occur less often. In this manner, normally-distributed returns are more statistically similar to market returns than uniformly random returns. In fact classical quantitative theory (after Bachelier) proposes that they are identical.

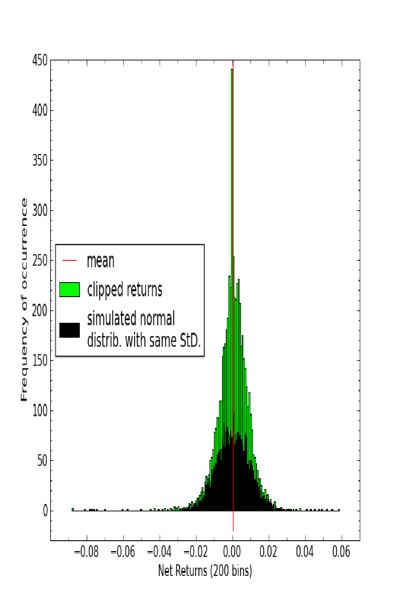

Decorrelation of Returns Figure 3 is an overlay of histograms of a normal distribution with that of the returns dataset. It clearly illustrates that the returns are not normally distributed: more returns are bunched around the mean and in the tails of the market net returns distribution than in a normal distribution.

Figure 3. A overlay of a histogram of the clipped net returns (green), with a histogram of a simulated normal distribution with the same mean, standard deviation and number of datum (black).

As a final comparison, a sonification of a statistically identical but decorrelated dataset to the net returns is presented. While they both appear to have short trending auto-correlative sequences, those of the net returns appear more consistently and when they do they appear to last for longer periods of time.

Summary Snapshots As a summary, here is 4 snippets of sonifications of the four datasets presented in this overview.

A. Uniformly distributed random data. B. Normally distributed random data. C. XAO Net Returns data. D. Decorrelated XAO Net Returns data.